Who will pay ESI contribution

Dr. Tanmoy Mukherji

Advocate

Who will pay ESI contribution-

Tanmoy Mukherji

Advocate

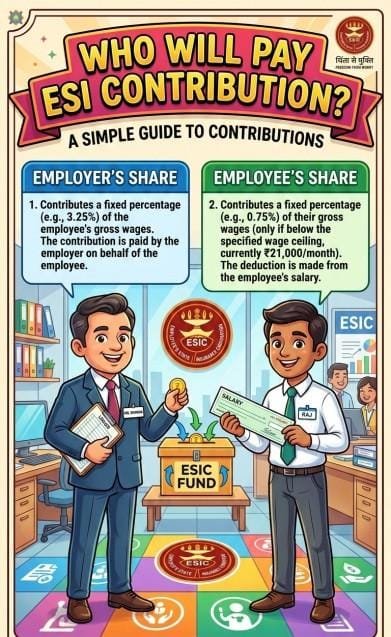

Employer pays both shares initially

Employer’s share – 3.25%

Employee’s share – 0.75%

→Employer deducts employee’s share from wages and deposits the total with ESIC.

→Legal responsibility is only on the employer, even if wages are unpaid

In case of contract labour

→Principal Employer (factory owner / establishment head) is responsible.

→He may recover the contractor’s share later, but ESIC payment cannot be delayed.

→Section 40, ESI Act, 1948.

When should ESI be paid?

→Time limit

→ESI contribution must be paid on or before the 15th day of the following month

Example:

January salary → ESI paid by 15th February

March salary → ESI paid by 15th April

Who files returns?

Employer files online monthly contribution return on the ESIC portal showing:

→Employee details

→Wages

→Contributions paid

“The employer shall pay both employer’s and employee’s contribution to ESIC.”

“Contribution must be paid on or before 15th of the succeeding month.”

“Principal employer is liable in case of contract labour.”

ESI calculation when salary is ?21,000

ESI is applicable up to ?21,000 per month

Rates:

→Employer’s share: 3.25%

→Employee’s share: 0.75%

→Total: 4%

Calculation:

Employer = 3.25% of 21,000

= ?682.50

Employee = 0.75% of 21,000

= ?157.50

Total ESI contribution:

?682.50 + ?157.50 = ?840 per month

On which salary is ESI calculated?

ESI is calculated on GROSS WAGES, not just basic salary.

Gross wages include:

→Basic pay

→Dearness allowance (DA)

→HRA

→Overtime wages

→Incentives & bonuses (monthly)

→Meal allowance (if paid in cash)

Not included:

→Washing allowance

→Annual bonus

→Retrenchment compensation

→Gratuity

→Leave encashment

ESI contribution is calculated on gross wages payable, excluding specified exclusions under the ESI Act.

Example

If an employee earns ?18,000 gross salary:

Employer (3.25%) = ?585

Employee (0.75%) = ?135

Total ESI = ?720 per month

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.