RULE AGAINST PERPETUITY

The Transfer of Property Act, 1882

TANMOY MUKHERJI INSTITUTE OF JURIDICAL SCIENCE

Dr. Tanmoy Mukherji

Advocate

RULE AGAINST PERPETUITY [Section 14 of the Transfer of Property Act, 1882]-

Tanmoy Mukherji

Advocate

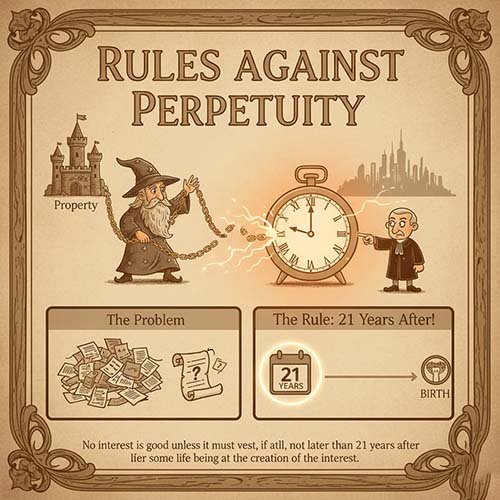

Section 14 of the Transfer of Property Act deals with 'the Rule against perpetuity'. It is an extended provision of Section 13.

Meaning-

The word 'Perpetuity' means, "tying up property for an indefinite period or forever". "Perpetual enjoyment' means, "enjoyment forever". Section (14) of the T.P.Act corresponds to Section (114) of the Indian Succession Act, 1925, which runs as follows-

No transfer of property can operate to create an interest which is to take effect after the lifetime of one or more persons living at the date of such transfer, and the minority of some person who shall be in existence at the expiration of that period, and to whom, if he attains full age, the interest created is to belong.

Section 114 Indian Succession Act-

"No bequest is valid whereby the vesting of the thing bequeathed may be delayed beyond the lifetime of one or more persons living at the expiration of that period, and to whom, if he attains full age, the thing bequeathed is to belong."

Jarman defines perpetuity as "a perpetuity in the primary sense of the word is a disposition, which makes property inalienable for an indefinite period".

Principle-

- There are some persons, who wish to retain their properties in their own family from generations to generations perpetually. But it is the policy of the law to prevent the creation of perpetuities. Property cannot be tied up longer than for a life in being and beyond minority. This rule/principle is called 'the Rule against perpetuity'.

-The policy of law has been to prevent property from being tied up forever. The rule against perpetuity has been founded on the general policy that liberty of alienation shall not be exercised to its own destruction and all contrivances which tend to create perpetuity or place property forever out of the reach of the exercise of the power of alienation shall be void.

Perpetuity may arise in two ways-

(1) By taking away from the owner of property the power of alienation thereof; and

(2) By creating future remote interest in the property.

The former case is covered by Section 10 of this Act and the latter is covered by this section.

-The object of the rule against perpetuity is to restrain the creation of future conditional interest in property.

Ingredients:-

To attract Section 14, the following conditions are to be satisfied-

(i)There should be a transfer of property.

(ii) Interest so created must take effect after the lifetime of one or more persons living at the date of such transfer and during the minority of the unborn person.

(iii) Transfer should be to create an interest in favor of an unborn person.

(iv) The unborn person should be in existence at the expiration of the interest of the living persons.

Perpetuity period-

Perpetuity period is one in which one cannot postpone the vesting of property in transferee beyond certain limit. It is the period of which vesting of interest may lawfully be postponed. Under this rule, the maximum period during which, the owner of the property can control its flow is prescribed.

Analysis of the Rule-

(1) The vesting cannot be postponed beyond the lifetime of any one or more persons living at the date of the transfer. For example, if an estate is given to a living person, A for life, then to a living person, B for life and then to the unborn son of B. Here the son of B must be in existence on or before the date of the expiry of the life estate in favor of B.

-Stated in another way, the rule amounts to saying that, except in case of minority, discussed below, there must be no interest between the termination of the preceding interest of a living person and the vesting of the interest taken by the person who was not in existence at the date of the transfer.

(2) The vesting of absolute interest in favor of an unborn person may be postponed until he attains full age. For example, an estate may be transferred to A, a living person, and after his death to his unborn son when he attains the age of 18. Such a transfer would not be violative of the rule against perpetuity.

The extent of perpetuity period-

The perpetuity period, that is to say, the maximum period during which the property may be rendered inalienable, is the life of any person who is, or of the survivor of any number of persons who are alive at the moment when the deed which creates the interest begins to operate, plus a period of 18 years from the time when such designated person dies. For example, the owner of a property may transfer it to a living person, A, for life, and after his death to B, a living person, for life, and on or before B's death to his unborn son when he attains the age of 18. Suppose A remains alive for 10 years; B for 15 years and the unborn son comes into existence just before the death of B. As the unborn son would not get the property until he attains the age of 18, it follows that the property would remain tied up for 33 years.

Extent of perpetuity period: Position in India-

-Life or any number of lives in being + period of gestation + minority period of the unborn beneficiary.

Example-

Assume that A, B, C are the life estate holders who enjoyed the property. In that A enjoyed for 15 years, then B enjoyed for 20 years and C enjoyed for 10 years and died then the unborn person came into existence. Now perpetuity period is-

A -B -C - M.P

15+20+10+18= 63 years.

In this case if the vesting of an absolute interest to an unborn person is more than 63 years, that is void on the basis of the 'rule against perpetuity'.

Example-

A, B, C are the life estate holders who enjoyed the property. In that A enjoyed 15 years, then B enjoyed 20 years and C also enjoyed 10 years at the end of which the unborn person conceived and came into existence 150 days after the death of C. Now the perpetuity period is-

A + B + C + P.G + M.P.

15 + 20 + 10 + 150 days + 18 years

Here the perpetuity period is 63 years and 150 days. So, vesting of property is more than 63 years and 150 days. It is void.

English Law-

Life or lives in being + period of gestation + minority period.

If we apply this rule to the above example, the perpetuity period is-

15 + 20 + 10 + 21 = 66 years

15 + 20 + 10 + 280 days + 21 = 66-280

Difference between English Law and Indian Law-

|

English Law

|

Indian Law

|

|

1. Minority period is 21 years.

|

1. It is 18 years.

|

|

2. Period of gestation is a gross period.

|

2. It should be actual period.

|

|

3. Property need not be given absolutely to unborn person.

|

3. It should be given absolutely.

|

|

4. The unborn person must come into existence within 21 years of the death of last life estate holder.

|

4. He must come into existence before the death of the last life estate holder.

|

Exceptions to the rule against perpetuity-

The rule against perpetuity allows the following exceptions-

(i)Public Charitable Trust-

The rule does not apply in case of transfer for the benefit of the public i.e. advancement of religion, knowledge, commerce, health and safety.

(ii) Covenants of Redemption-

This rule does not offend the covenants of redemption in mortgage.

(iii) Personal Agreements-

It does not apply when the transfer creates only a personal obligation and does not affect the interest in the property.

(iv) Agreement for Pre-emption-

Agreements for Pre-emption gives first as option to purchase land since the agreement to purchase does not cast any interest in the property. So this rule does not apply to the agreement or pre-emption.

(v) Provision for the Payment of the Debts of the Transferor- When a direction is given that the income of the property shall be accumulated for the payment of debts and it does not tie up the property totally because the person indebted can discharge the debt at any time.

(vi) Perpetual Lease-

It is also not applicable to the contracts of perpetual renewal of leases.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.