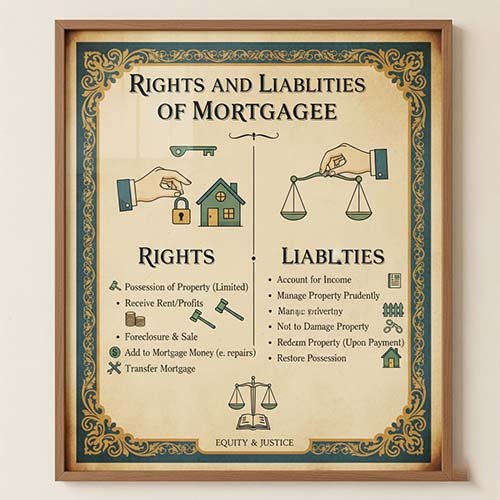

RIGHTS AND LIABILITIES OF MORTGAGEE

The Transfer of Property Act, 1882

TANMOY MUKHERJI INSTITUTE OF JURIDICAL SCIENCE

Dr. Tanmoy Mukherji

Advocate

RIGHTS AND LIABILITIES OF MORTGAGEE [Sections 67 - 77 of the Transfer of Property Act, 1882] –

Tanmoy Mukherji

Advocate

Sections 67 to 77 of the Transfer of Property Act, 1882 lay down the provisions relating to the rights and liabilities of the Mortgagee as detailed below.

The term 'foreclosure' literally means, "to take legal measures to terminate a mortgage and to take possession of the mortgaged property. A mortgagor under Section 60 is entitled to the right of redemption. Section 67 provides for corresponding right, the right of foreclosure or sale to the mortgagee. Right to Foreclosure means that when the mortgagor's right to redeem has become complete and he has failed to avail himself thereof, the mortgagee has the right to apply to the court for a decree that the mortgagor shall be absolutely debarred of his right to redeem the mortgaged property.

Section 67 runs as follows-

Foreclosure is the method by which the mortgagee acquires the property freed from the mortgagor's right of redemption. That means, it gives rights to the mortgagee to institute a suit for foreclosure or sale in default by the mortgagee to institute a suit for the deed for payment has arrived, there is no question of foreclosure that would arise. If the mortgagor has paid or deposited the mortgage money, or if a decree for redemption is made, the mortgagee is not entitled to exercise the right of foreclosure or sale.

Right of Sale-

Right of sale means right of the mortgagee to apply to the court for the sale of mortgaged property for satisfaction of his debt.

Difference between Foreclosure and the Right of Sale-

(a) By means of foreclosure, the mortgagee becomes the absolute owner by the property and mortgage debt is absolutely discharged, whereas by means of judicial sale, mortgagee realizes the actual value of the property and can recover balance, if the sale proceeds are not sufficient to satisfy the mortgage debt.

(b) Foreclosure is possible only by suit, whereas sale is possible either out of court or by means of suit.

2. Mortgagee when bound to bring one suit on several mortgages (Section 67A)-

A mortgagee who holds two or more mortgages executed by the same mortgagor in respect of each of which he has a right to obtain the same kind of decree under Section 67, and who sues to obtain such decree on any one of the mortgages, shall, in the absence of a contract to the contrary, be bound to sue on all the mortgages in respect of which the mortgage money has become due.

3.Right to sue for mortgage money (Section 68)-

Section 68 has been redrafted by the Amending Act 20 of 1929.

It runs as follows-

(1) The mortgagee has a right to sue for the mortgage money in the following cases and in no others, namely:

(a) Where the mortgagor binds himself to repay the same;

(b) Where, by any cause other than the wrongful act or default of the mortgagor or mortgagee, the mortgaged property is wholly or partially destroyed or the security is rendered insufficient within the meaning of Section 66, and the mortgagee has given the mortgagor a reasonable opportunity of providing further security enough to render the whole security sufficient, and the mortgagor has failed to do so;

(c) Where the mortgagee is deprived of the whole or part of his security by or in consequence of the wrongful act or default of the mortgagor;

(d) Where, the mortgagee being entitled to possession for the mortgaged property, the mortgagor fails to deliver the same to him, or to secure the possession thereof to him without disturbance by the mortgagor or any person claiming under a title superior to that of the mortgagor;

Provided that, in the case referred to in Clause (a), a transferee from the mortgagor or from his legal representative shall not be liable to be sued for the mortgage money.

(2) Where a suit is brought under Clause (a) or Clause (b) of sub section (1), the Court may, at its discretion, stay the suit and all proceedings therein, notwithstanding any contract to the contrary, until the mortgagee has exhausted all his available remedies against the mortgaged property or what remains of it, unless the mortgagee abandons his security and, if necessary, retransfer the mortgaged property.

4. Power of sale when valid (Section 69)-

Section 69 deals with the power of a mortgagee to sell the mortgaged property without the intervention of the Court.

It runs as follows-

1) A mortgagee, or any person acting on his behalf, shall, subject to the provisions of this section have power to sell or concur in selling the mortgaged property or any part thereof, in default of payment of the mortgage money, without the intervention of the Court, in the following cases and in no others, namely-

(a) Where the mortgage is an English mortgage, and neither the mortgagor nor the mortgagee is a Hindu, Mohammedan or Buddhist or a member of any other race, sect, tribe or class from time to time specified in this behalf by the State Government, in the Official Gazette;

(b) Where a power of sale without the intervention of the Court is expressly conferred on the mortgagee by the mortgage deed, and the mortgagee is the Government;

(c) Where a power of sale without the intervention of the Court is expressly conferred on the mortgagee by the mortgage deed, and the mortgaged property or any part thereof was, on the date of the execution of the mortgage deed, situate within the towns of Calcutta, Madras, Bombay, or in any other town or area which the State Government may, by notification in the Official Gazette, specify in this behalf.

2) No such power shall be exercised unless and until -

(a) Notice in writing requiring payment of the principal money has been served on the mortgagor, or on one of several mortgagors, and default has been made in payment of the principal money, or of part thereof, for three months after such service; or

(b) Some interest under the mortgage amounting at least to five hundred rupees is in arrears and unpaid for three months after becoming due.

3) When a sale has been made in professed exercise of such a power, the title of the purchaser shall not be impeachable on the ground that no case had arisen to authorize the sale, or that due notice was not given, or that the power was otherwise improperly or irregularly exercised; but any person damnified by an unauthorized or improper or irregular exercise of the power shall have his remedy in damages against the person exercising the power.

4) The money which is received by the mortgagee, arising from the sale, after discharge or prior encumbrances, if any,, to which the sale is not made subject, or after payment into Court under Section 57 of a sum to meet any prior encumbrance, shall, in the absence of a contract to the contrary, be held by him in trust to be applied by him first, in payment of all costs, charges and expenses properly incurred by him as incident to the sale or any attempted sale; and, secondly, in discharge of the mortgage money and costs and other money, if any, due under the mortgage; and the residue of the money so received shall be paid to the person entitled to the mortgaged property, or authorized to give receipt for the proceeds of the sale thereof.

Nothing in this section or in Section 69A applies to powers conferred before the first day of July 1882.

5. Appointment of receiver (Section 69A)-

Section 69.A, inserted by the Amending Act 20 of 1929 empowers the mortgagee (who can exercise a power of sale under Section 69, T.P.Act) to appoint a Receiver.

It runs as follows-

(1) A mortgagee having the right to exercise a power of sale under Section 69 shall, subject to the provisions of sub section (2), be entitled to appoint, by writing signed by him or on his behalf, a receiver of the income of the mortgaged property or any part thereof.

(2) Any person who has been named in the mortgage deed and is willing and able to act as receiver may be appointed by the mortgagee.

-If no person has been so named, or if all persons named are unable or unwilling to act, or are dead, the mortgagee may appoint any person to whose appointment the mortgagor agrees; failing such agreement, the mortgagee shall be entitled to apply to the Court for the appointment of a receiver, and any person appointed by the Court shall be deemed to have been duly appointed by the mortgagee.

-A receiver may at any time be removed by writing signed by or on behalf of the mortgagee and the mortgagor, or by the Court on application made by either party and on due cause shown.

-A vacancy in the office of receiver may be filled in accordance with the provisions of this sub section.

(3) A receiver appointed under the powers conferred by this section shall be deemed to be the agent of the mortgagor; and the mortgagor shall be solely responsible for the receiver's acts or defaults, unless the mortgage deed otherwise provides or unless such acts or defaults are due to the improper intervention of the mortgagee.

(4) The receiver shall have power to demand and recover all the income of which he is appointed receiver, by suit, execution or otherwise, in the name either of the mortgagor or of the mortgagee to the full extent of the interest which the mortgagor could dispose of, and to give valid receipts accordingly for the same, and to exercise any powers which may have been delegated to him by the mortgagee, in accordance with the provisions of this section.

(5) A person paying money to the receiver shall not be concerned to inquire if the appointment of the receiver was valid or not.

(6) The receiver shall be entitled to retain out of any money received by him, or for his remuneration, and in satisfaction of all costs, charges and expenses incurred by him as receiver, a commission at such rate not exceeding five per cent, on the gross amount of all money received as is specified in his appointment, and, if no rate is so specified, then at the rate of five per cent on that gross amount, or at such other rate as the Court thinks fit to allow, on application made by him for that purpose.

(7) The receiver shall, if so directed in writing by the mortgagee, insure to the extent, if any, to which the mortgagee might have insured and keep insured against loss or damage by fire, out of the money received by him, the mortgaged property or any part thereof being of an insurable nature.

(8) Subject to the provisions of this Act as to the application of insurance money, the receiver shall apply all money received by him as follows, namely-

(i) In discharge of all rents, land revenue, rates and out goings whatever affecting the mortgaged property;

(ii) In keeping down all annual sums or other payments, and the interest on all principal sums, having priority to the mortgage in right whereof he is receiver;

(iii) In payment of his commission, and of the premiums on fire, life or other insurances, if any, properly payable under the mortgage deed or under this Act, and the cost of executing necessary or proper repairs, directed in writing by the mortgagee;

(iv) In payment of the interest falling due under the mortgage;

(v) In or towards discharge of the principal money, if so directed in writing by the mortgagee;

-and shall pay the residue, if any, of the money received by him to the person who, but for the possession of the receiver, would have been entitled to receive the income of which he is appointed receiver, or who is otherwise entitled to the mortgaged property.

(9) The provisions of the sub section (1) apply only if and as far as a contrary intention is not expressed in the mortgage deed; and provisions of sub sections (3) to (8) inclusive may be varied or extended by the mortgage deed, and, as so varied or extended, shall, as far as may be, operate in like manner and with all the like incidents, effects and consequences, as if such variations or extensions were contained in the said sub sections.

(10) Application may be made, without the institution of a suit, to the Court for its opinion, advice or direction on any present question respecting the management or administration of the mortgaged property, other than questions of difficulty or importance not proper in the opinion of the Court for summary disposal. A copy of such application shall be served upon, and the hearing thereof may be attended by, such of the persons interested in the application, as the Court may think fit.

-The costs of every application under this sub section shall be in the discretion of the Court.

(11) In this section, 'the Court' means the Court, which would have jurisdiction in a suit to enforce the mortgage.

6.Accession to mortgaged property (Section 70)-

If, after the date of a mortgage, any accession is made to the mortgaged property, it corresponds to Section 63, which deals with the mortgagor's right to accessions.

Section 70 runs as follows-

If, after the date of a mortgage, any accession is made to the mortgaged property, the mortgagee, in the absence of a contract to the contrary, shall, for the purposes of the security, be entitled to such accession.

Illustrations-

(a) A mortgages to B a certain field bordering on a river. The field is increased by alluvion. For the purposes of his security, B is entitled to the increase.

(b) A mortgages a certain plot of building land to B and afterwards erects a house on the plot. For the purposes of his security, B is entitled to the house as well as the plot.

7. Renewal of mortgaged lease (Section 71)-

When the mortgaged property is a lease, and mortgagor obtains a renewal of the lease, the mortgagee, in the absence of a contract to the contrary, shall, for the purposes of the security, be entitled to new lease.

8. Rights of mortgagee in possession (Section 72)-

A mortgagee may spend such money as is necessary-

(a) For the preservation of the mortgaged property from destruction, forfeiture or sale;

(b) For supporting the mortgagor's title to the property;

(c) For making his own title thereto good against the mortgagor; and

(d) When the mortgaged property is renewable leasehold, for the renewal of the lease;

-and may, in the absence of a contract to the contrary, add such money to the principal money, at the rate of interest payable on the principal, and, where no such rate is fixed, at the rate of nine percent per annum.

-Provided that the expenditure of money by the mortgagee under Clause (b) or Clause (c) shall not be deemed to be necessary unless the mortgagor has been called upon and has failed to take proper and timely steps to preserve the property or to support the title.

-Where the property is by its nature insurable, the mortgagee may also, in the absence of a contract to the contrary, insure and keep insured against loss or damage by fire the whole or any part of such property; and the premiums paid for any such insurance shall be added to the principal money with interest at the same rate as is payable on the principal money or, where no such, rate is fixed, at the rate of nine percent per annum. But the amount of such insurance shall not exceed the amount specified in this behalf in the mortgage deed or (if, no such amount is therein specified), two thirds of the amount that would be required in case of total destruction to reinstate the property insured.

-Nothing in this section shall be deemed to authorize the mortgagee to insure when an insurance of the property is kept up by or on behalf of the mortgagor to the amount in which the mortgagee is hereby authorized to insure.

9.Right to proceeds of revenue sale or compensation on acquisition (Section 73)-

Where the mortgaged property or any part thereof or any interest therein is sold owing to failure to pay arrears of revenue or other charges of a public nature or rent due in respect of such property, and such failure did not arise from any default of the mortgagee, the mortgagee shall be entitled to claim payment of the mortgage money, in whole or in part, out of any surplus of the sale proceeds remaining after payment of the arrears and of all charges and deductions directed by law.

-Where the mortgaged property or any part thereof or any interest therein is acquired under the Land Acquisition Act, 1894 (1 of 1894); or any other enactment for the time being in force providing for the compulsory acquisition of immovable property, the mortgagee shall be entitled to claim payment of the mortgage money, in whole or in part, out of the amount due to the mortgagor as compensation.

-Such claims shall prevail against all other claims except those of prior encumbrancers, and may be enforced notwithstanding that the principal money on the mortgage has not become due.

Section 74 & 75 –

Repealed by Section 39 of the Transfer of Property (Amendment) Act (XX of 1929).

10. Liabilities of mortgagee in possession (Section 76)-

When, during the continuance of the mortgage, the mortgagee takes possession of the mortgaged property-

(a) He must manage the property as a person of ordinary prudence would manage it if it were his own;

(b) He must try his best to collect the rents and profits thereof;

(c) He must, in the absence of a contract to the contrary, out of the income of the property, pay the Government revenue, all other charges of a public nature and all rent accruing due in respect thereof during such possession, and any arrears of rent in default of payment of which the property may be summarily sold;

(d) He must, in the absence of a contract to the contrary, make such necessary repairs of the property as he can pay for out of the rents and profits thereof after deducting from such rents and profits, the payment mentioned in Clause (c) and the interest on the principal money;

(e) He must not commit any act which is destructive or permanently injurious to the property;

(f) Where he has insured the whole or any part of the property against loss or damage by fire, he must, in case of such loss or damage, apply any money which he actually receives under the policy, or so much thereof as may be necessary, in reinstating the property, or, if the mortgagor so directs, in reduction or discharge of the mortgage money;

(g) He must keep clear, full and accurate accounts of all sums received and spent by him as mortgagee, and, at any time during the continuance of the mortgage, give the mortgagor, at his request and cost, true copies of such accounts and of the vouchers by which they are supported;

(h) His receipts from the mortgaged property, or, where such property is personally occupied by him, a fair occupation rent in respect thereof, shall, after deducting the expenses properly incurred for the management of the property and the collection of rents and profits and the other expenses mentioned in Clauses (c) and (d), and interest thereon, be debited against him in reduction of the amount (if any), from time to time due to him on account of interest, and, so far as such receipts exceed any interest due, in reduction or discharge of the mortgage money; the surplus, if any, shall be paid to the mortgagor;

(i) When the mortgagor tenders, or deposits in the manner hereinafter provided, the amount for the time being due on the mortgage, the mortgagee must, not withstanding the provisions in the other clauses of this section, account for his receipts from the mortgaged property from the date of the tender or from the earlier time when he could take such amount out of Court, as the case may be and shall not be entitled to deduct any amount therefrom on account of any expenses incurred after such date or time in connection with the mortgaged property.

Loss occasioned by his default-

If the mortgagee fails to perform any of the duties imposed upon him by this section, he may when accounts are taken in pursuance of a decree made under this Chapter, be debited with the loss, if any, occasioned by such failure.

11. Receipts in lieu of interest (Section 77)-

Nothing in Section 76, Clauses (b), (d), (g) and (h), apply to cases where there is a contract between the mortgagee and the mortgagor that the receipts from the mortgaged property shall, so long as the mortgagee is in possession of the property, be taken in lieu of interest on the principal money, or in lieu of such interest and defined portions of the principal.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.