The provisions of the Payment of Wages Act, 1936 with regard to deductions which may, and which may not, be deducted from wages

Dr. Tanmoy Mukherji

Advocate

The provisions of the Payment of Wages Act, 1936 with regard to deductions which may, and which may not, be deducted from wages

Tanmoy Mukherji

Advocate

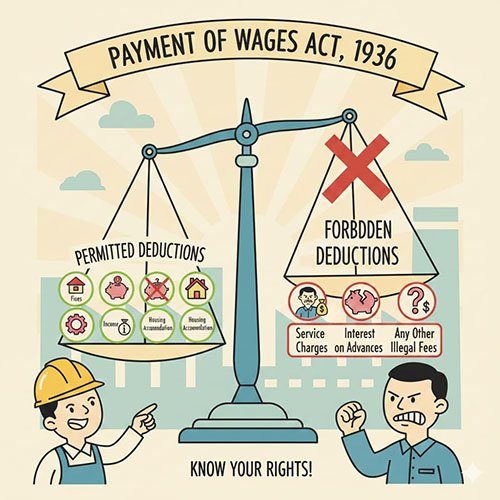

→The Payment of Wages Act, 1936 was enacted to regulate the payment of wages to certain classes of employed persons and to ensure that wages are paid without unauthorized deductions.

Section 7 of the Act is the controlling provision which lays down that wages shall be paid without deductions, except those expressly authorized by the Act.

General Rule Regarding Deductions (Section 7)-

→Wages of an employed person shall be paid without any deductions.

→Only deductions permitted under Section 7(2) can be made.

→Any deduction not covered under the Act is illegal and punishable.

Ref. Case-

A.V. D’Costa v. B.C. Patel (AIR 1955 SC 412)

The Supreme Court held that deductions from wages are strictly regulated, and employers cannot make deductions except as authorized by the Act.

Deductions Which May Be Deducted (Authorized Deductions)-

Deductions by Way of Fines (Section 8)

→Fines can be imposed only for acts or omissions approved by the employer.

→Must be recorded in a Register of Fines.

→Fine shall not exceed 3% of wages payable in a wage period.

→No fine can be imposed on an employee below 15 years of age.

Ref. Case

Macleod & Co. v. Their Employees (AIR 1962 SC 1543)

The Court held that fines must strictly comply with statutory requirements; otherwise, they are illegal.

Deductions for Absence from Duty (Section 9)-

→Deduction may be made for absence from duty.

→Proportionate deduction according to the period of absence.

→Includes absence due to participation in an illegal strike.

Ref. Case-

Bank of India v. T.S. Kelawala (1990) 4 SCC 744

The Supreme Court held that wages can be deducted for the period of absence due to strike, applying the principle of “no work, no pay.”

Deductions for Damage or Loss (Section 10)-

→Allowed only if damage or loss is caused by employee’s neglect or default.

→Employee must be given an opportunity to show cause.

→Deduction shall not exceed the actual amount of loss.

Ref. Case-

Burn & Co. Ltd. v. Their Workmen (AIR 1959 SC 529)

The Court ruled that deductions for loss without proof of employee’s negligence are invalid.

Deductions for House Accommodation (Section 7(2)(d))

→Permitted when house accommodation is provided by the employer.

→Must be authorised by State Government rules.

Ref. Case-

Khem Chand v. Union of India (AIR 1963 SC 687)

The Court observed that deductions for accommodation must be reasonable and authorized by law.

Deductions for Amenities and Services (Section 7(2)(e))

→Includes water, electricity, medical facilities, etc.

→Deductions must be voluntarily accepted by the employee.

Ref. Case

Manganese Ore (India) Ltd. v. Chandi Lal Saha (1991 Lab IC 1305)

The Court held that deductions without employee consent for amenities are illegal.

Deductions for Recovery of Advances and Loans (Section 7(2)(f) & (ff))-

→Recovery of advances given before or after employment is allowed.

→Recovery subject to prescribed conditions and limits.

Ref. Case

Bata Shoe Co. Ltd. v. D.N. Ganguly (AIR 1961 SC 1158)

The Supreme Court upheld lawful recovery of advances as per statutory rules.

Statutory Deductions (Section 7(2)(h))-

→Provident Fund

→Employees’ State Insurance (ESI)

→Income Tax

Ref. Case

Organo Chemical Industries v. Union of India (1979) 4 SCC 573

Statutory deductions are mandatory and do not amount to illegal deductions.

Deductions Pursuant to Court Orders (Section 7(2)(g))-

Deductions made under court decree or order for attachment of wages.

Ref. Case

Radhey Shyam v. State of UP (AIR 1969 All 504)

The Court held that deductions pursuant to judicial orders are valid.

Deductions Which May NOT Be Deducted (Unauthorised Deductions)-

The following deductions are strictly prohibited:

Deductions not mentioned under Section 7.

→Excessive or arbitrary fines.

→Deductions without giving the employee a chance to explain.

Deductions for:

→Normal wear and tear

→Employer’s business losses not caused by employee fault

→Deductions made as a punishment without legal sanction.

Ref. Case

M/s. Shree Meenakshi Mills Ltd. v. Labour Appellate Tribunal (AIR 1957 SC 49)

The Supreme Court held that unauthorized deductions violate the purpose of the Act.

The Payment of Wages Act, 1936 provides a comprehensive statutory framework to protect workers from unjust and arbitrary deductions. Section 7 clearly demarcates permissible and impermissible deductions, and courts have consistently enforced strict compliance to uphold workers’ wage security.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.