MORTGAGE: MEANING, DEFINITION AND KINDS OF CLASSIFICATION OF MORTGAGE

Transfer of Property Act, 1872

Dr. Tanmoy Mukherji

Advocate

MORTGAGE: MEANING, DEFINITION AND KINDS OF CLASSIFICATION OF MORTGAGE-

Tanmoy Mukherji

Advocate

Meaning-

"The expression 'Mortgage' literally means transfer of an interest by pleading (delivering) a property as security against an advance as loan; or an existing or future debt; or for performance of an act or engagement, which gives rise to liability". It is a transfer of limited interest of an immovable property as security against a loan, to another.

Section 58(a) of the Transfer of Property Act, 1882 defines the terms Mortgage, Mortgagor, Mortgagee, Mortgage money and Mortgage deed as follows:

According to Section 58(a) of the T.P.Act, 1882 A mortgage is a transfer of interest in specific immovable property for the purpose of security-

(a) The payment of money advanced or to be advanced by way of loan;

(b) An existing or future debt;

(c) The performance of an engagement which may give rise to a pecuniary liability.

-In mortgage, the transferor is called 'Mortgagor', the transferee is called 'Mortgagee', the interest secured is called 'Mortgage money' and the instrument/document in which mortgage is effected is called 'Mortgage deed'.

Mortgagor-

The person who actually mortgages the property is a mortgagor, but a new Section 59-A introduced by the Amendment Act 20 of 1929 says that a mortgagor includes a person deriving title under the original mortgagor. That section really refers to such persons as heirs, executors, and administrators, who derive their title from the mortgagor. For the purpose of Section 68 (a), however, the term mortgagor does not include the transferee of the mortgagor, for the transferee is not bound by the mortgagor’s personal covenant, though in Clause (c) of that section a subsequent purchaser would be included. Apart from this, the rules which apply to decide the competence of a person to be a transferor equally apply in the case of a mortgagor. Accordingly, when a mortgage is executed by several persons, some of whom are minors and some are pardanashin ladies who have not executed the deed in accordance with law, the execution is not invalid as regards the rest, and the mortgage is valid and binding on them. A mortgage by the minor, who is incompetent to contract, is void. The creditor cannot recover money even under Sections 64 and 65 of Contract Act in case of mortgage by a minor.

Mortgagee-

A mortgagee is a person in whose favour a mortgage is created. The term also includes, under the new Section 59-A a person deriving a title under the original mortgagee. Every mortgage deed must name, some person as a mortgagee, otherwise it cannot be a mortgage. Thus, a security bond given to the Court cannot be enforced as a mortgage, for the Court is not a judicial person. A mortgage executed in favour of a minor who has advanced the whole of the mortgage money is enforceable by him or by other person on his behalf.

Mortgage-money-

The expression 'mortgage-money' means "the principal money and interest of which payment is secured for the time being". Accordingly, a mortgagor cannot redeem the property on the repayment only of the principal money. He must also pay the interest thereon because the interest is regarded as a charge upon the property just as much as the principal amounts. The parties are, however, free to enter into any contract to the contrary. But the mere fact that the mortgagors make themselves personally liable for the payment of interest is not compatible with the interest is also forming a charge on the property. It must be noted that the interest is provided for by the terms of the mortgage-deed. Where no provision is made for it, the security will only be for the principal money.

Mortgage deed-

The definition of mortgage in Section 2 (17) of Stamp Act is wider than in Section 58 (a) of Transfer of Property Act. It includes pawn or pledge of movables and is not restricted to transfer of an interest or right to immovable property. It also includes charge, which creates a right to property.

Amendment-

The following amendments have been made by the Amending Act 20 of 1929-

(i) A proviso has been inserted in Section 58(c).

(ii) Section 58 (d) has been made more exhaustive by the inclusion of the case where the mortgagee is entitled to appropriate a portion only of the income of property mortgaged in payment of the mortgage money.

(iii) Clause (f) and (g) have been newly added. The Act recognized a mortgage by deposit of title deeds in Section 59 and an anomalous mortgage in Section 98, but there was no definition of such mortgages before.

Elements of Mortgage-

Mortgage constitutes the following elements-

1. Transfer of Interest.

2. Specific Immovable Property.

3. Security.

4. Consideration or purpose.

5. Competence of parties; and

6. Registration.

1. Transfer of Interest-

In Mortgage, only an interest in property is transferred. The word transfer of interest signifies that the interest, which passes to the mortgagee is not ownership or dominion, which notwithstanding the mortgage resides in the mortgagor. The right of mortgagee is only an accessory right, which is intended merely to secure the due payment of a debt.

2. Specific Immovable Property-

The subject matter of mortgage must be a specific immovable property. It must be distinctly specified. The property described in the mortgage deed should be properly identified. Further, the word 'specific' is to be distinguished from the word 'general'. For instance my house and land are said to be vague and general.

3. Security-

The purpose of pleading the property is to provide security of payment or performance of work or clearance of a debt.

4. Consideration-

Consideration exists in mortgage. Every mortgage must be supported by consideration, which means something in return. The mortgagor mortgages the property in consideration of some advance or an existing or future debt or in performance of an engagement-giving rise to pecuniary liability.

5. Competence of parties-

The parties namely, Mortgagor and Mortgagee must be competent to contract. (Within the meaning of Section 11 of the Indian Contract Act, 1872). Further, the mortgagor must have a title or authority to transfer.

6. Registration (Section 59)-

Registration is necessary if the value of the property is Rs.100/- and above. It is optional, if the value is below Rs.100/-. The registered instrument (if any) is to be signed by the transferor and attested by two witnesses.

Kinds or Classification of Mortgages (Section 58(b) to (g)-

Section 58(b) to (g) of the T.P.Act deal with different kinds of mortgages as follows-

(1) Simple Mortgages [Section 58(b)].

(2) Mortgage by Conditional Sale (Sections 58(c)).

(3) Usufructuray Mortgage (Sections 58(d) & 62 ).

(4) English Mortgage [Section 58(e)].

(5) Mortgage by deposit of Title deeds or Equitable Mortgage (Sections 58(f) & 96); and

(6) Anomalous Mortgage [Section 58(g)].

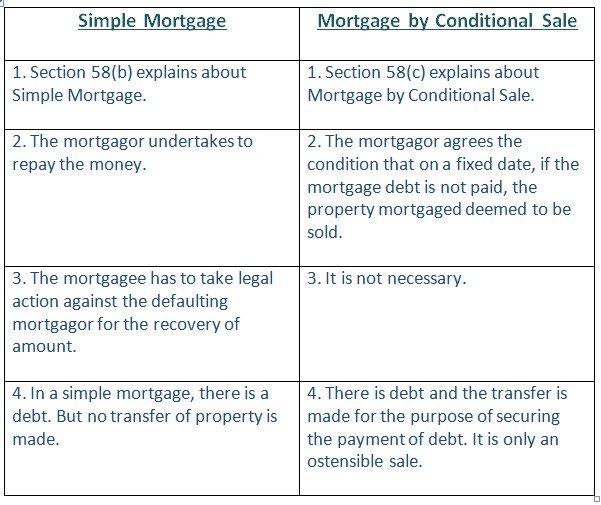

(1) Simple Mortgage [Section 58(b)]-

Section 58(b) speaks about Simple Mortgage. It runs as follows-

Where, without delivering possession of the mortgaged property, the mortgagor binds himself personally to pay the mortgage money, and agrees, expressly, or impliedly, that, in the event of his failing to pay according to his contract, the mortgagee shall have a right to cause the mortgaged property to be sold and the proceeds of sale to be applied, so far as may be necessary, in payment of the mortgage money, the transaction is called a simple mortgage and the mortgagee a simple mortgagee.

-In this case, there is a transfer of interest. But the possession of the property is retained by Mortgagor. The mortgagee binds himself to pay.

Conditions:

To constitute simple mortgage, the following conditions are to be satisfied-

(i) The mortgagor retains the possession of the mortgaged property;

(ii) The mortgagor must personally undertake to pay the mortgage money; and

(iii) The parties must expressly or impliedly agree that in the event of the mortgagor, failing to pay according to his contract, the mortgagee shall have a right to cause the mortgage property to be sold.

Remedies-

In simple mortgage, the Mortgagee will have the following remedies-

(i) He can get the property sold through court in case of default;

(ii) A suit can be instituted in 12 years form the date when the amount falls due.

Registration is compulsory irrespective of the mortgage amount.

(2) Mortgage by Conditional Sale (Section 58(c)-

Section 58(c) deals with Mortgage by Conditional Sale. It runs as follows-

Where the mortgagor ostensibly sells the mortgaged property-

i) On condition that on default of payment of the mortgage money on a certain date the sale shall become absolute; or

ii) On condition that on such payment being made the sale shall become void; or

iii) On condition that on such payment being made the buyer shall transfer the property to the seller;

The transaction is called a mortgage by conditional sale.

Provided that no such transaction shall be deemed to be a mortgage, unless the condition is embodied in the document, which effects or purports to effect to the sale.

-In this case, mortgage appears to be a sale. But the sale is ostensible, not real. The transfer of interest in the property is effected subject to the following conditions-

(i) The mortgagor ostensibly sells the mortgaged property.

(ii) He sells the property on condition that:

(a) On payment of mortgage money the sale shall become void, and the buyer shall transfer the property to the seller on the date fixed;

(b) On default of payment of the mortgage money on the date fixed, the sale shall become absolute.

(iii) The conditions, which effect or purport to effect the sale, must be embodied in the document of transfer.

The condition is embodied (enshrined) in the instrument/deed/document.

-The world 'ostensible' in Section 58 (c) has two meanings -

(i) That the object bears a certain form or appearance without suggesting that it is or is not that of which it has the superficial appearance; and

(ii) That the object bears a certain appearance but, is not really that of which it bears the appearance.

To decide whether a transaction is a mortgage by conditional sale or an outright sale, its true nature has got to be determined by the intention of the parties thereto as evidenced by the terms of the document.

Registration-

Registration is necessary if the mortgage money exceeds Rs. 100/-

Distinction between A 'Simple Mortgage' and 'Mortgage by Conditional Sale'-

(3) Usufructuary Mortgage [Section 58(d)]-

Section 58(d) of the T.P.Act provides for 'Usufructuary Mortgage'.

It runs as follows-

Where the mortgagor delivers possession or expressly or by implication binds, himself to deliver possession of the mortgaged property to the mortgagee, and authorizes him to retain such possession until payment of the mortgage money, and to receive the rents and profits accruing from the property or any part of such rents and profits and to appropriate the same in lieu of interest, or in payment of the mortgage-money, or partly in lieu of interest or partly in payment of the mortgage, money, the transaction is called an usufructuary mortgage and the mortgagee as usufructuary mortgagee.

-In the case, possession is transferred to mortgagee. Mortgagee gets rents, profits etc., against the property in lieu of interest or principal or both. The mortgagee has no remedy except enjoyment of property.

Condition-

To constitute usufructuary mortgage, the following conditions are to be satisfied-

(i) Possession of the property is delivered to the mortgagee;

(ii) The mortgagee is to get rents and profits in lieu of interest or principal or both;

(iii) No personal liability is incurred by the mortgagor; and

(iv) The mortgagee cannot foreclose or sue for sale.

Registration is necessary if the amount is Rs.100/- or above.

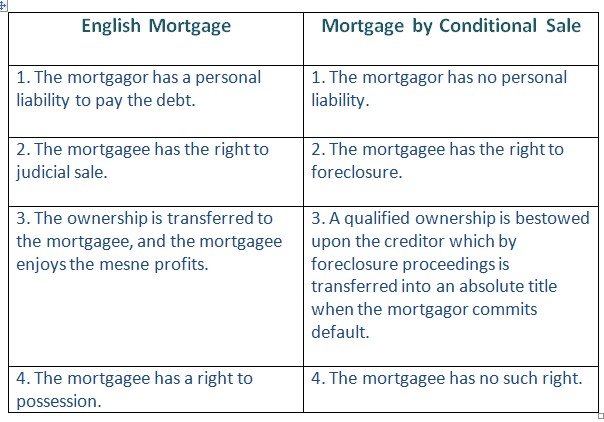

(4) English Mortgage [Section 58(e)]-

Section 58(e) of the T.P.Act makes provision for English Mortgage.

It runs as follows-

Where the mortgagor binds himself to repay the mortgage money on certain date, and transfers the mortgaged property absolutely to the mortgagee, but subject to a proviso that he will retransfer it to the mortgagor upon payment of the mortgage money as agreed, the transaction is called an English mortgage.

-In English mortgage, the mortgagor binds himself to pay the mortgage money on a certain date, and transfers the property (immovable) to the mortgagee subject to retransfer on repayment of mortgage money.

Characteristic Features-

Following are the characteristic features of the English mortgage-

(i) That the mortgagor should bind himself to repay the mortgage money on a certain day;

(ii) That the mortgaged property should be transferred absolutely to the mortgagee; and

(iii) That such absolute transfer should be made subject to a proviso that the mortgagee will reconvey the property to the mortgagor, upon payment by him of the mortgage money on the appointed day.

-The general rule in respect of registration (Rs.100/- or above) and the period of limitation (12 years) are applicable for the English Mortgage also.

Distinction between English Mortgage and Mortgage by Conditional Sale-

(5) Mortgage by Deposit of Title Deeds or Equitable Mortgage (Section 58(f)-

Section 58(f) of the T.P.Act provides for the Mortgage by deposit of title deeds.

It runs as follows-

Where a person in any of the following towns, namely, the towns of Calcutta, Madras and Bombay, and in any other town which the State Government concerned may, by notification in the Official Gazette, specify in this behalf, delivers to a creditor or his agent documents of title to immovable property, with intent to create a security thereon, the transaction is called a mortgage by deposit of title deeds.

-In this case, Title deed of the immovable property is transferred to mortgagee. Transfer of one important document is enough. (All documents/deeds need not be transferred). This type of mortgage is effected in major towns like Madras, Bombay, Calcutta or those notified by the Government.

Essential features-

Following are the essential features of the Mortgage by deposit of title deeds-

(i) A debt;

(ii) Deposit of the title deeds; and

(iii) An intention that the deeds shall be security for the debt.

Distinction between Mortgage by Conditional Sale and Mortgage by Deposit of Title Deeds-

|

Mortgage by Conditional Sale

|

Mortgage by Deposit of Title deed

|

|

1. It is explained in Section 58(c).

|

1. It is explained in Section 58(f).

|

|

2. It is an ostensible sale.

|

2. It is an equitable mortgage.

|

|

3. Generally, the property is transferred to mortgagee.

|

3. Generally, the property is retained by the mortgagor only.

|

|

4. There is no restriction on territorial jurisdiction.

|

4. There is a restriction on territorial jurisdiction.

|

|

5. The mortgagor has no personal liability to pay the debt.

|

5. The mortgagor has a personal liability to pay the debt.

|

|

6. A qualified ownership is bestowed upon the creditor which by foreclosure proceedings is transformed into an absolute title when the mortgagor commits default.

|

6. The mortgagee is entitled to judicial process to recover the debt.

|

|

7. Registration is necessary.

|

7. Registration is not necessary. Mere writing, along with handing over the title deeds is sufficient.

|

(6) Anomalous Mortgage [Section 58(g)]-

Section 58(g) of the T.P.Act speaks about Anomalous mortgage.

It runs as follows:

A mortgage which is not a simple mortgage, a mortgage by conditional sale, an usufructuary mortgage, an English mortgage or a mortgage by deposit of title deeds within the meaning of this section is called an anomalous mortgage.

-Anomalous mortgage is one, which does not come within the purview of any one of the mortgages as stated above. It is a combination of the two or more mortgages as stated/discussed above.

Example-

Kanom, Otti, Peruartham of Madras and san mortgage of Gujarat are the examples of the Anomalous mortgage.

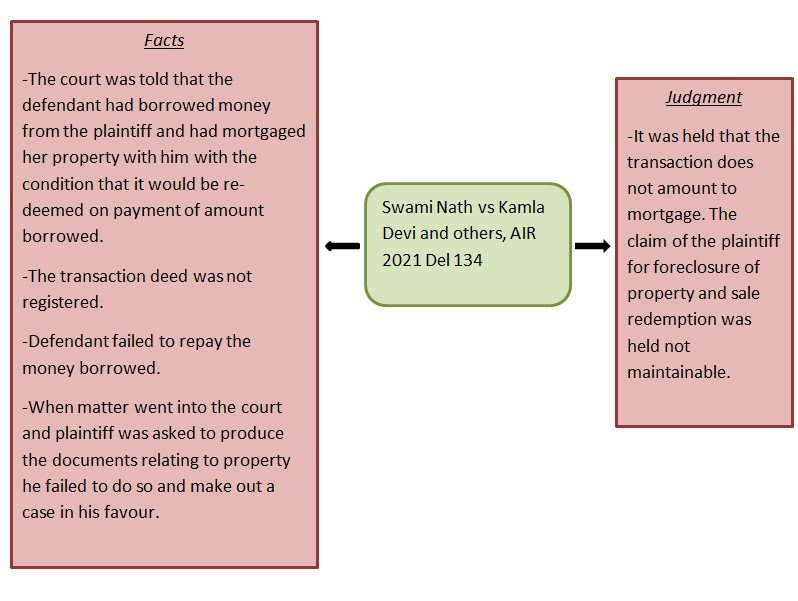

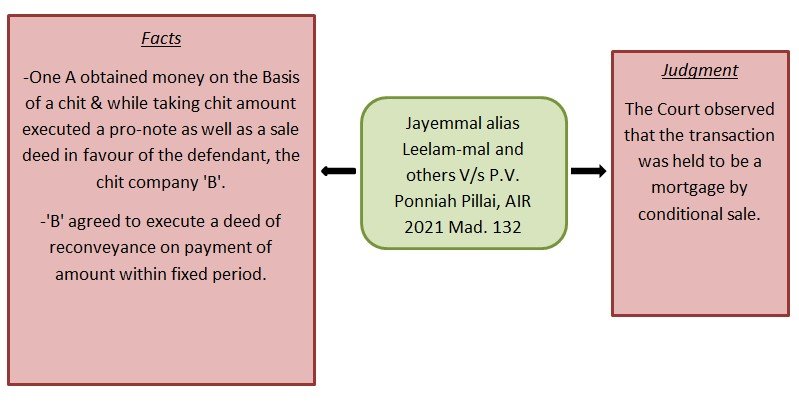

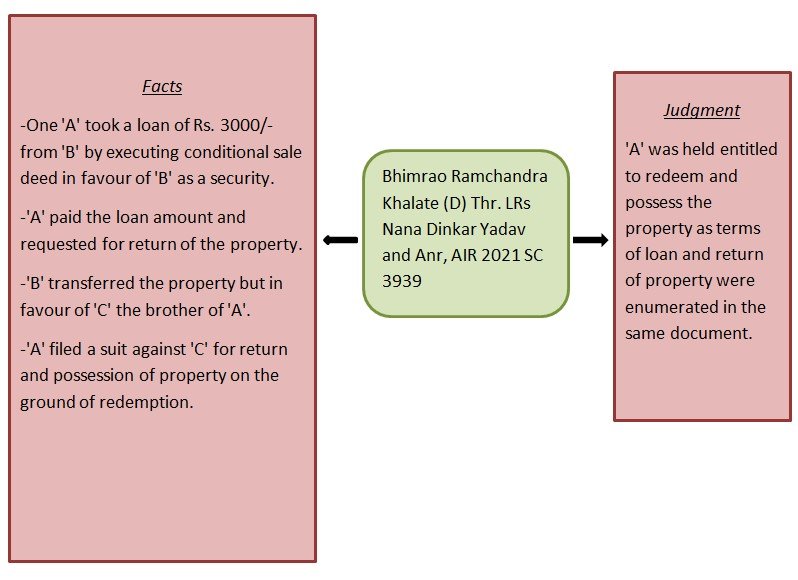

Recent Judicial Developments-

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.