Development of GST Law in India

Dr. Tanmoy Mukherji

Advocate

Development of GST Law in India-

Tanmoy Mukherji

Advocate

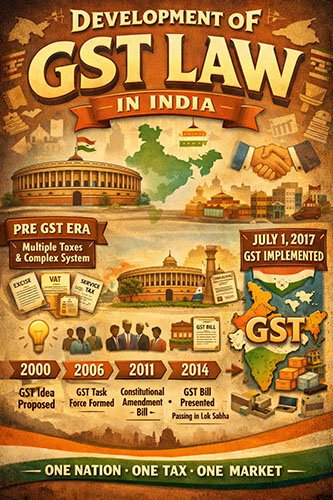

The Goods and services Tax (GST) introduced in India on 1st July, 2017, is a landmark indirect tax reform aimed at creating a unified National Market by subsuming multiple central and state taxes. Since its implementation, GST has been treated as a dynamic and evolving law, undergoing continuous changes to address practical difficulties, revenue concerns and constitutional issues.

Background/History -

India followed a dual indirect tax system where both Centre and state levied taxes independently.

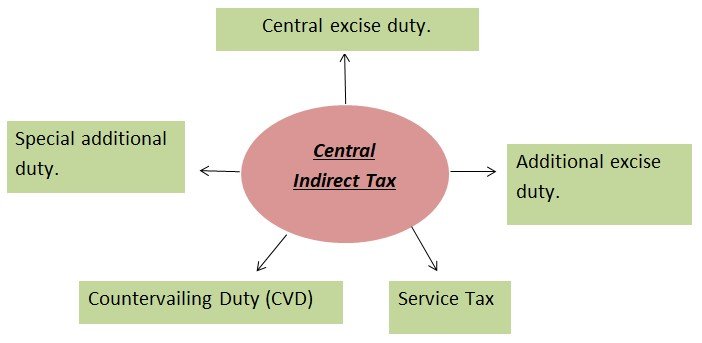

i) Central Indirect Tax-

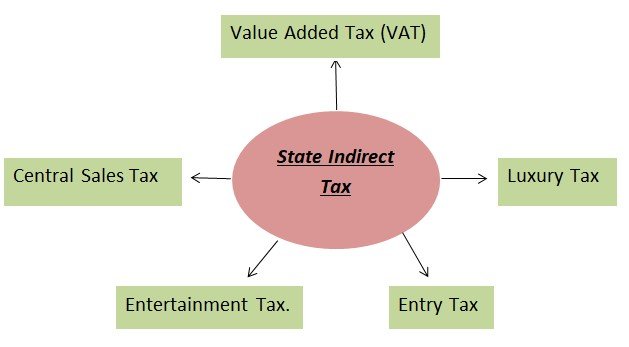

ii) State Indirect Tax-

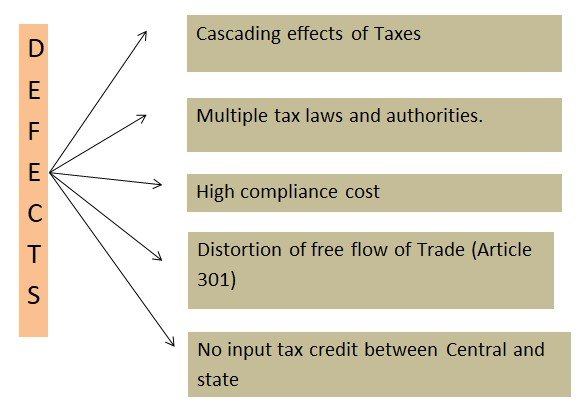

Defects of Pre-GST Regime-

GST Concept-

GST is a destination based, value added, consumption tax levied on supply of Goods and Services.

Features-

1. Single tax replacing multiple indirect taxes.

2. Seamless Input Tax Credit (ITC).

3. Taxation at point of consumption.

4. Technology driven compliance.

5. Dual GST model (Centre + State).

Steps towards GST-

Kelkar Task Force (2003)-

→Recommended integration of goods and services taxation.

→Suggested abolition of cascading taxes.

→Proposed GST as a comprehensive solution.

VAT Implementation-

→Replaced sales Tax.

→Reduced cascading within states only.

→Could not integrate central taxes.

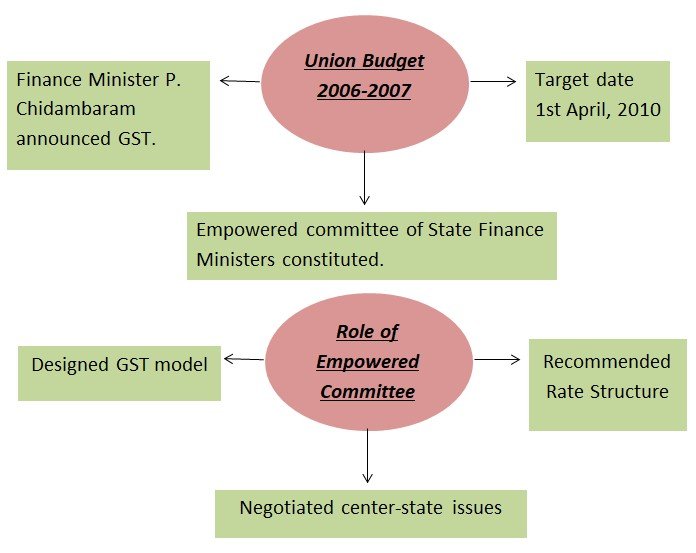

Budget Announcement and Industrial Framework-

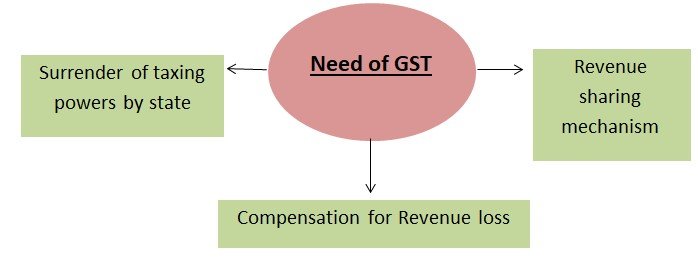

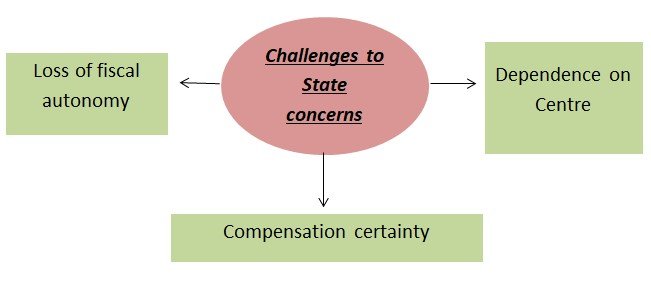

Federal Challenges in implementing GST-

Constitutional Amendment Process-

122nd Constitutional Amendment Bill, 2014-

→ Introduction in Lok Sabha.

→ Passed by Parliament in 2016.

→ Ratified by more than 50% of State.

101st Constitutional Amendment Act, 2016-

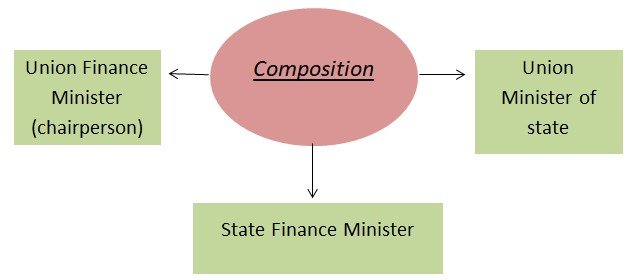

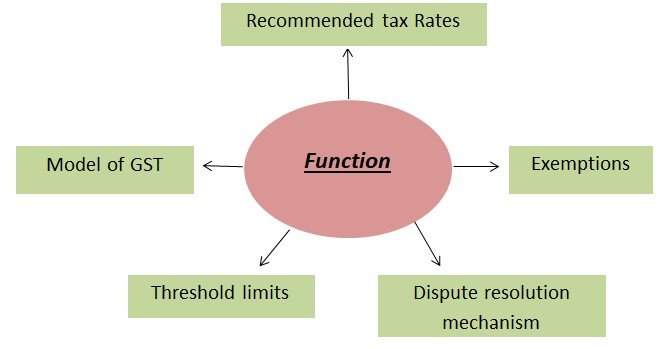

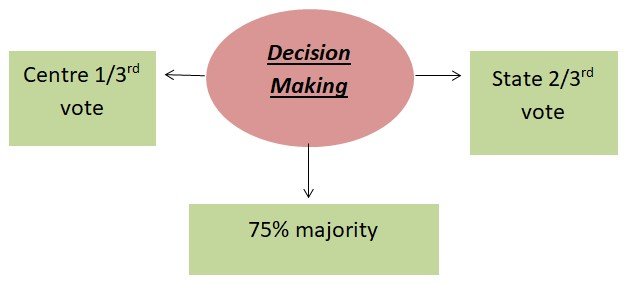

GST Council –

Enactment of GST Legislation (2017)-

→ CGST, 2017

→ IGST, 2017

→ UGST, 2017

→ GST Compensation Act, 2017

State laws-

Individual SGST Acts passed by the states.

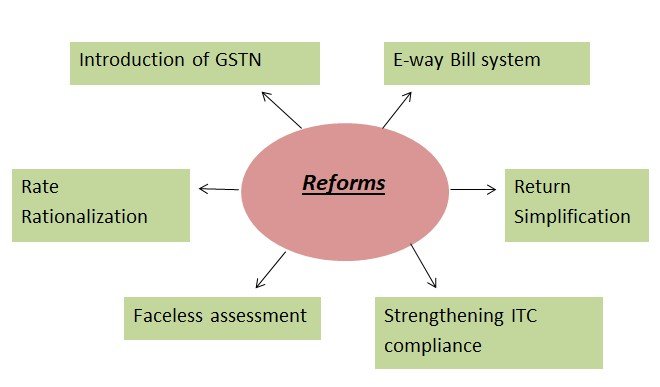

Post-GST Reforms and development-

GST 2.0 Majors overhaul of GST Regime (From 22nd September, 2025)-

The most significant recent change in GST law is the launch of "GST 2.0", a wide-ranging reform implemented after 56th GST Council meeting (held on 3rd Sept. 2025).

-This reforms are the largest since GST was introduced in 2017.

Simplification of GST Rate Structure-

The old multi-slab GST rate system (5%, 12%, 18%, and 28%) has been simplified-

5% → Merit/Essential goods

18% → Standard Rate for most goods and Services

40% → Special Luxury Rate on selected goods (Tobacco).

Exemption & Nil / Low Tax -

→Life insurance

→Health insurance

→Life-saving medicine and medical devices have been moved to Nil or 5% GST.

→FMCG and daily use items - 5%

→Electronics - 18%

→Small cars and auto parts - GST lower to 18%.

we believe in a holistic approach to legal education building not just lawyers, but socially conscious leaders of tomorrow.